(SINGPORE 2026.3.31)At the start of this year, German global auto parts giant Bosch reached an agreement with worker representatives at its Waiblingen plant in Germany to wind down production by the end of 2028, directly affecting 560 employees. Production will be relocated to China and Thailand, and by 2030, Bosch’s total job reductions in Germany are projected to reach 20,000.

The decision has drawn attention, with some framing it as a retreat from Germany. Yet both industry observers and company statements stress that Bosch’s restructuring reflects strategic adaptation to global market trends rather than a forced exodus.

The move exemplifies a wider transformation sweeping the automotive industry. Electrification, digitalization, and China’s emergence as a dominant EV market are reshaping the car industry’s traditional supply chains. German suppliers are responding by scaling back certain domestic operations while expanding in Asia, particularly China, where demand for electric vehicles (EVs) and related technologies is surging, according to a column in China’s tech news platform 36 Kr.

Other German peers ZF, Continental, and Schaeffler are making similar adjustments, increasing investment, production, and R&D in China to stay competitive, noted the column Zhejieju (正解局).

Founded in 1887, Bosch first improved the electromagnetic ignition system and has since amassed over 70,000 patents, many defining global standards. The company has pioneered advances in autonomous driving, Industry 4.0, hydrogen energy, and electrification. Today, two out of every three cars worldwide contain core Bosch components. While Bosch never manufactured vehicles itself, it shaped the internal combustion engine (ICE) era, becoming a dominant supplier across global automotive value chains.

Despite this legacy, Bosch faces new pressures. Preliminary 2025 results show its core mobility division generated €56 billion (about S$83 billion) in revenue, comprising over 60% of group sales, yet profitability declined, with an annual cost gap of about €2.5 billion. Chairman Stefan Hartung called 2025 “a difficult year,” highlighting structural realignments within Germany.

The Waiblingen closure and planned restructuring at other German sites are responses to market realities. But they do not signify abandonment of Germany, Reuters noted. By 2030, Bosch plans to cut around 13,000 additional German jobs, mainly in mobility, adding to 9,000 layoffs announced in 2024, for a total of about 22,000. By the end of 2025, Bosch’s global workforce has fallen to 412,400, with its German force experiencing the sharpest cut.

These reductions target older facilities with underused capacity in a move to align resources with global demand and profitability pressures. Two main factors drive this realignment: high domestic production costs and evolving demand. Labour costs in Germany are over three times higher than in China, and electricity, land, and other overheads are substantially more expensive.

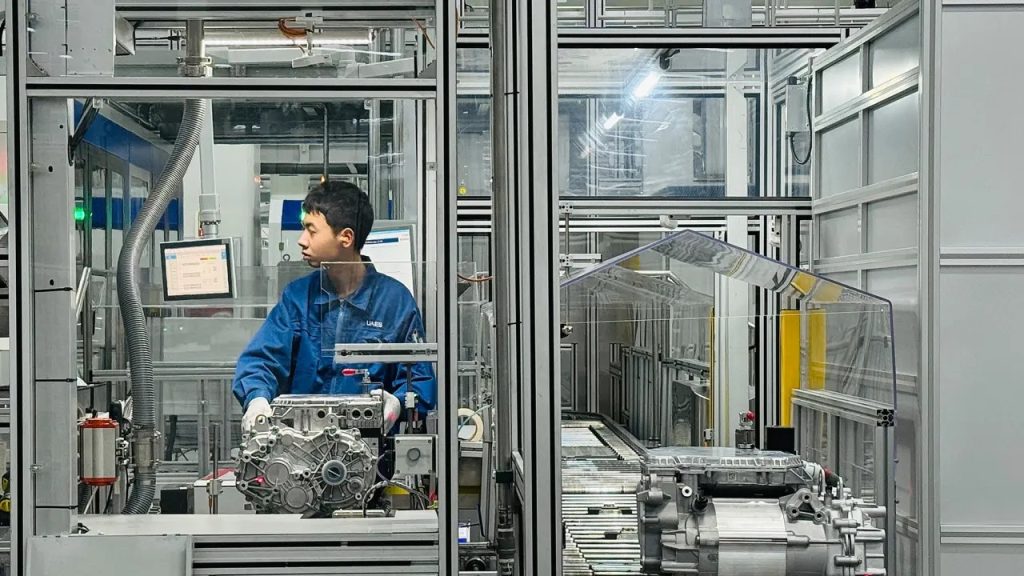

The automotive sector is shifting away from ICE vehicles, which rely heavily on engines, transmissions, and connectors like those produced at Waiblingen. EVs prioritize batteries, electric drivetrains, thermal management, and intelligent control chips. Domain controllers and integrated wiring systems have replaced many traditional components, and the “three electric systems” (battery, motor, control) now account for over 70% of an EV’s cost. Consequently, demand for conventional parts in Europe has declined, leaving some of Bosch’s facilities underutilized despite ongoing R&D.

Bosch’s situation mirrors broader European trends. Between 2024 and 2025, Europe’s auto parts sector cut over 104,000 jobs, with German companies accounting for a substantial share. ZF plans 11,000–14,000 cuts in Germany by 2028; Schaeffler will eliminate 4,700 positions; and Continental aims to reduce more than 10,000 with plant closures.

But relocating production to China and Thailand is not a refuge. Bosch continues to invest in Germany, maintaining major R&D, production, and administrative operations. Its expansion in China, however, aims to tap the world’s largest automotive market: in 2025, China produced and sold about 34 million vehicles, and Bosch’s China sales rose 4.9% to 149.8 billion yuan (about S$28.5 billion). Localization in high-demand markets is standard practice for multinationals.

Other German firms also fixate on China. ZF has secured major EV orders in the country; Schaeffler’s electrification business in Asia-Pacific is growing rapidly; and Continental has established China-based R&D centers. China’s integrated supply chain—from lithium mining to vehicle assembly—offers scale and cost advantages that Germany cannot match short-term.

China controls about 65% of the global power battery market, with CATL (宁德时代) holding 39.2%, while BYD dominates electric drivetrains and Huawei and Horizon Robotics (地平线机器人) lead in advanced driving chips. High localization rates deliver efficiencies in logistics, labour, and R&D. Bosch is also investing €2.5 billion in artificial intelligence by 2027, focusing on China’s EV and smart mobility sector.

The industry-wide restructuring underscores a pivotal reality: the ICE era, which Bosch helped define, is ending. Electrification has shifted value toward new systems and technologies. Integration with China’s supply chain is now essential to remain competitive. Even Volkswagen is developing China-specific EVs with local partners.

Bosch’s trajectory illustrates the challenges and opportunities for legacy industrial firms in a rapidly transforming global landscape, Reuters pointed out. Plant closures, layoffs, and geographic shifts are deliberate steps to stay competitive, embrace the EV era, and secure a sustainable future in which China plays a central role. The global automotive industry has entered a new era, and Bosch is recalibrating to thrive—anchored in Germany, yet fully engaged worldwide through China.

Meanwhile, Japan’s Denso, the world’s second biggest auto parts company after Bosch, has been present in China for decades and continues to strengthen its operations there as part of its global manufacturing and market strategy. Canada’s Magna International, the third largest, has been increasing its presence in China for many years and is continuing to grow there, especially in electrification and local partnerships.

In the 11 months to November in 2025, German investments in China reached a four‑year high of over €7 billion, up about 55% from 2024 and 2023 levels, according to data analyzed by Reuters. German investments remain one of China’s largest FDI.