For the past two decades, returns from equities and bonds have been negatively correlated; when one goes up, the other goes down. This has been to the benefit of multi-asset investors, who have been able to reduce portfolio risks and limit losses in times of market distress.

However, the current macroeconomic and policy backdrop raises some questions about whether this regime can continue.

Indeed, the first few weeks of 2022 highlighted this concern, with both equities and bonds selling off. Could this be a sign of things to come?

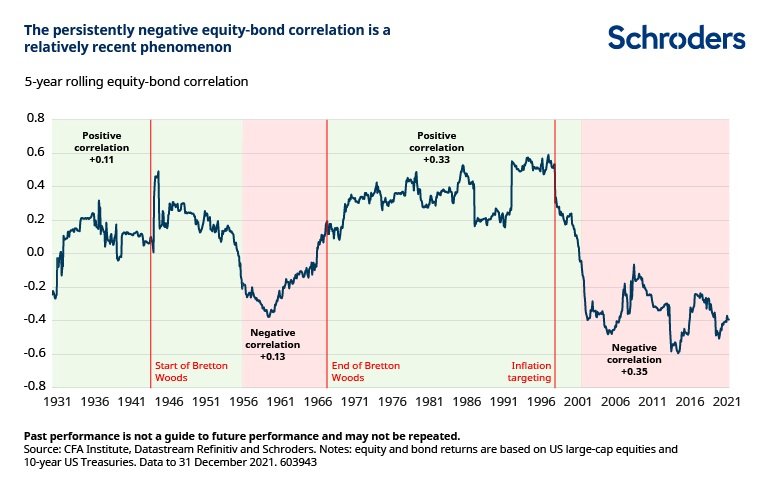

Well, for a start, let’s not forget that negative equity-bond correlations are a relatively new phenomenon. Between 1931-1955 and 1970-1999, the five-year correlation was mostly positive.

Our analysis reveals what market factors investors should monitor for signs of a permanent change in the equity-bond correlation.

Breaking down equity-bond correlations

Bond and equity prices reflect the discounted value of their future cash flows, where the discount rate approximately equals the sum of a:

- Real interest rate – compensation for the time value of money

- Inflation rate – compensation for the loss of purchasing power over time

- Risk premium – compensation for the uncertainty of receiving future cash flows

While bonds pay fixed coupon payments, some equities offer the potential to pay and increase dividends over time and so will also incorporate a dividend growth rate.

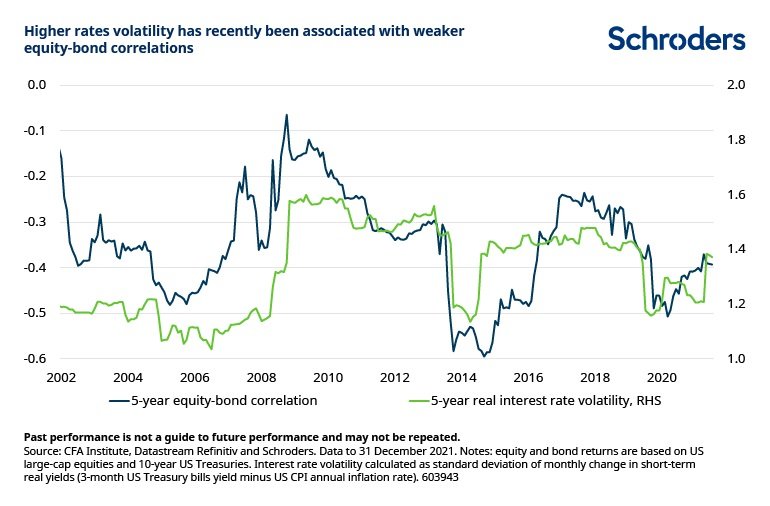

Higher interest rate volatility

An increase in real interest rates affects both equities and bonds in the same direction by increasing the discount rate applied to future cash flows.

Although this unequivocally hurts bond prices, the impact on equity prices is more ambiguous and will depend (among other factors) on the degree of risk appetite.

For example, if rates rise alongside an increase in economic uncertainty, risk appetite should decrease. This is as investors demand a higher risk premium to compensate for the uncertainty of receiving future cash flows – a net negative for equity prices.

But if rates rise alongside a decrease in economic uncertainty, risk appetite should increase as investors demand a lower risk premium – a net positive for equities.

In general, large interest rate fluctuations introduce additional uncertainty into the economy by making it more difficult for consumers and businesses to plan for the future, which in turn lowers investor risk appetite.

So all else being equal, higher rate volatility should be negative for both bonds and equities, meaning positive equity-bond correlations.

The below chart exemplifies this point: since the early 2000s, the equity-bond correlation has closely followed the level of real rates volatility.

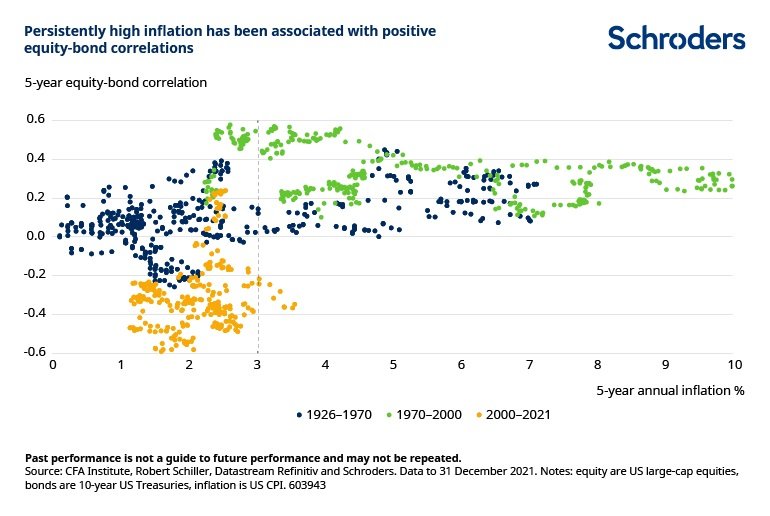

Higher inflation

Bonds are an obvious casualty from rising inflation. Their fixed stream of interest payments become less valuable as inflation accelerates, sending yields higher and bond prices lower to compensate.

Meanwhile, the effect on equities is once again less straightforward. In theory, a rise in prices should correspond to a rise in nominal revenues and therefore boost share prices.

On the other hand, the market may discount those future earnings at a higher rate when inflation rises, as they are worth less in today’s money.

It is therefore the net impact of higher expected nominal earnings versus higher discount rates that determines how equities behave in an environment of rising inflation.

Our analysis finds that the discount effect tends to dominate when inflation exceeds 3% a year on a five-year basis.

This is illustrated in the next chart: since 1926, the equity-bond correlation has been positive 98% of the time whenever inflation breached this threshold.

Stagflation

When risk appetite is low, investors tend to sell equities and buy bonds for downside protection. But when risk appetite is high, investors tend to buy equities and sell bonds.

This “risk-on, risk-off” behaviour causes equity and bond risk premia to regularly diverge and is supportive of a negative equity-bond correlation.

However, if risk appetite is lacking because investors are worried about both slowing growth and high inflation (i.e. stagflation), they may dislike all assets that promise future cash flows and prefer cash instead, inducing a positive equity-bond risk premia relationship.

This is exactly what manifested during the 1970s when the US economy was facing economic difficulties and high levels of inflation.

Summary

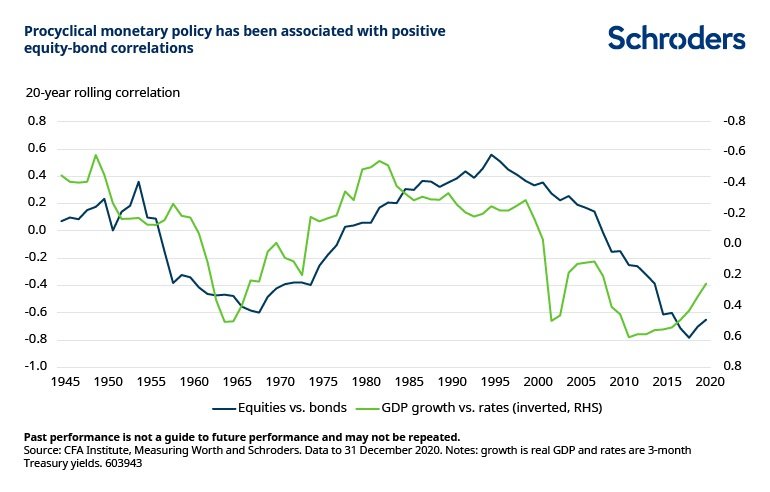

When interest rates and inflation are high and volatile, risk premia are moving in the same direction and monetary policy is procyclical, equity-bond correlations are more likely to be positive.

In contrast, when interest rates and inflation are low and stable, risk premia are moving in the opposite direction and monetary policy is countercyclical, equity-bond correlations are more likely to be negative.

Complicating matters further, the relative importance of these factors is not constant, but varies over time.

So what does this framework tell us about the prospect of a regime change? Well, some of the factors that have supported a negative equity-bond correlation may be waning.

In particular, inflation has risen to multi-decade highs and its outlook is arguably also highly uncertain. This could spell more rate volatility as central banks withdraw stimulus to cool the economy.

Taken together, conviction over a continuation of the negative equity-bond correlation of the past 20 years should at least be questioned.